Yutaka Okada, Senior Managing Executive Officer of Japan Securities Finance, shares with SFT the importance of the findings regarding the use of distributed ledger technology in the securities finance market.

Japan Securities Finance (JSF) has contributed to the development of Japan’s securities and financial markets for many years as Japan’s only securities finance company. Recognizing its public role as market infrastructure, JSF is also working to expand its frontiers, including conducting empirical research on how distributed ledger technology (DLT) can be applied to securities finance. It is working.

How do the services provided by JSF contribute to the market as a securities finance company?

JSF is a securities finance company established in 1950 under the Financial Instruments and Exchange Act. Our core business is margin trading financing, and we have played an important role as an infrastructure centering on the provision of liquidity in the Japanese securities market, particularly as a lender of last resort. We have been providing stock market solutions for over 70 years, and we also offer a variety of securities finance services to meet the diverse needs of our customers.

What is JSF doing regarding the use of DLT?

In collaboration with Professor Kenji Tanaka’s laboratory at the Graduate School of Engineering, the University of Tokyo, we will conduct empirical research to explore the feasibility of facilitating securities finance transactions (SFT) using DLT, and will publish a report summarizing the results in 2023. Announced on May 30th. .

Looking at the scale of Japan’s SFTs, the balance is approximately 200 trillion yen. However, in Japan, almost no research using DLT focusing on SFT has been conducted. It would be of great value to explore the possibility of using digital tokens in SFT, which is essential to providing liquidity to the market. Therefore, JSF decided to conduct this empirical study.

How did you conduct this research and what were the key findings?

The empirical study addressed three main research points.

The first is the feasibility of SFT for individual bilateral transactions. JSF has verified whether various SFTs, including the exchange of assets denominated in different currencies, can be carried out smoothly from the start of the transaction after a margin call to the end of the transaction. In addition to securities-for-cash exchanges (regular repos), we also tested securities-for-security exchanges.

The second evaluation focused on system performance in processing transactions at market size. Trades occurring across the market were entered into the system and its performance was evaluated. We analyzed how resilient the developed system is when trading is concentrated during times of market stress or recovery from system failures. Furthermore, we measured the ability to withstand large-scale system loads that are expected to occur during daily market value evaluations and margin calls, which are considered to result in large system loads.

The third research focus was on the impact of collateral diversification and margin call thresholding on net credit and liquidity requirements, including the impact during market turbulence.

We conducted simulations for each market scenario of sharp rises, sharp declines, and high volatility during normal times and during market turmoil, depending on the diversity of collateral and the presence or absence of thresholds for margin calls.

What impacts have you identified in your research and what are the benefits of using tokenized assets for SFT?

From this study, we drew five major conclusions.

Feasibility of the transaction

We have confirmed that various SFTs can be implemented smoothly from the start of transactions through margin calls to the end of transactions.

Regarding trade initiation, the recording and approval process ran smoothly, even during times of market stress when daily market-wide trades were concentrated in one hour. Even assuming that one-third of the outstanding transactions in the market as a whole were concentrated, it was possible to carry out mark-to-market valuation and margin call processing, although it would take a certain period of time.

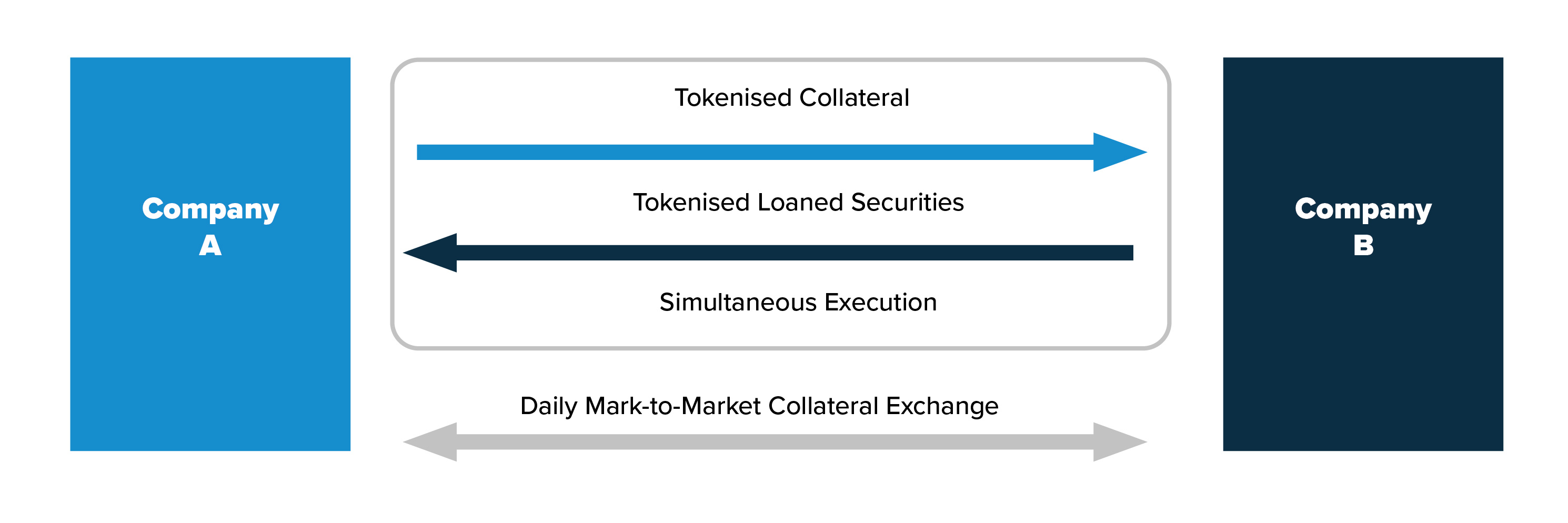

Figure 1: Conceptual diagram of empirical research

Reduction of settlement risk and simultaneous execution of transactions denominated in different currencies

By utilizing blockchain technology, tokens can be exchanged simultaneously without any time lag. For exchanges with existing payment systems involving foreign currencies or foreign securities, the transfer of funds or securities must be carried out at a local remittance institution during local time. For this reason, there is generally a time lag between the completion of transaction settlement and margin call.

In this empirical study, when recording and confirming transactions on the blockchain after a transaction, it is possible to simultaneously exchange tokens on the blockchain in real time, even if the underlying assets are denominated in different currencies. Additionally, margin calls can be automatically executed after daily market price updates without requiring any action from the trading parties.

Flexibility in credit risk mitigation and liquidity savings

The project confirmed that automating margin calls using blockchain technology can reduce operational burdens, make margin calls easier, and, as a result, reduce credit risk.

Automation can virtually eliminate the operational burden associated with managing collateral diversification and reconciling multiple assets pledged as collateral for margin calls. As a result, collateral diversification reduces not only the collateral value but also the volatility of the net credit amount, which has a positive effect on credit risk management. If thresholds are set to reduce the operational burden associated with margin calls, the automation provided through blockchain and smart contracts is itself critical in reducing operational burden. Therefore, setting a threshold also has the advantage of controlling the load on the system as the number of margin calls increases.

If you set a threshold, margin calls will not be executed until the net credit amount reaches the threshold. Therefore, the net credit amount increases compared to when no threshold is set. We found that this effect can be reduced or offset by diversifying collateral securities.

Furthermore, the credit risk reduction and liquidity saving effects of this combination of thresholds and collateral diversification were found to be particularly effective during market turmoil.

Improve operational efficiency

By using blockchain in SFT, payments can be automatically executed without human intervention according to the conditions set by smart contracts. This captures details related to the opening and closing of trades and margin calls during the trading period.

These results suggest that the use of blockchain enables straight-through processing (STP), making it possible to improve the efficiency of SFT operations and manage operational risks. In particular, it will be possible to significantly reduce the operational burden and time required to exchange transaction information with overseas trading partners and confirm the status of contracts, thereby increasing the efficiency of transactions.

Utilization of illiquid assets

Transferring the rights of securities with low liquidity, such as unlisted stocks, requires physical transfer and changes to the register, which may require a significant administrative burden and time. Tokenization facilitates the transfer of rights to illiquid assets. This creates the possibility of not only holding these illiquid assets but also using them as collateral for SFTs. Furthermore, as the amount used as collateral increases in this way, it is thought that the valuation of the underlying asset may rise.

The results of this research have been published as a paper “Empirical research on SFT using distributed ledger technology” (https://www.jsf.co.jp/media/report_dlt_ja.pdf).

What future work is planned regarding the use of DLT in SFT?

Through this research, we found various possibilities for leveraging blockchain to support SFT. Although there are issues such as connection with external systems and legal considerations, we would like to explore the possibility of actual transactions on a trial basis.

Is there anything else you would like to share with our readers?

In November 2023, JSF formulated and announced a long-term management vision that incorporates the corporate message “Be unique. Be unique.” Be a pioneer. ” We aim and strive to be unique and pioneers in the field of DLT.

We also actively participate in international conferences sponsored by the International Securities Lending Association (ISLA) and the Pan Asian Securities Lending Association (PASLA). We look forward to having stimulating discussions with market participants on this occasion.