return on equity.")

Finding a business with significant growth potential isn’t easy, but it’s possible if you focus on a few key financial metrics. In an ideal world, companies would invest more capital in their operations, and ideally the return on that capital would also increase. This shows that it is a compounding machine and the earnings can be continuously reinvested into the business to generate higher profits.However, when I looked into it, Sally Beauty Holdings (NYSE:SBH), we believe the current trend is outside the multibagger mold.

What is return on capital employed (ROCE)?

In case you aren’t familiar, ROCE is a metric that measures how much pre-tax profit (as a percentage) a company earns on the capital invested in its business. To calculate this metric for Sally Beauty Holdings, use the following formula:

Return on Capital Employed = Earnings before interest and tax (EBIT) ÷ (Total assets – Current liabilities)

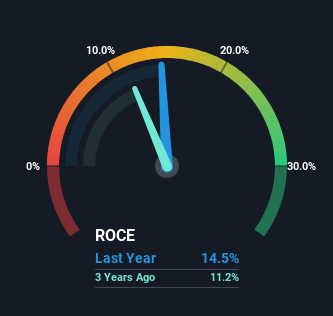

0.14 = USD 312 million ÷ (USD 2.7 billion – USD 573 million) (Based on the previous 12 months to December 2023).

So, Sally Beauty Holdings’ ROCE is 14%. This is a fairly standard return and in line with the industry average of 14%.

Check out our latest analysis for Sally Beauty Holdings.

Above you can see how Sally Beauty Holdings’ current ROCE compares to its previous return on capital, but history can only tell us so much. If you’re interested, take a look at our analyst forecasts. free Sally Beauty Holdings analyst report.

What are the return trends like?

When we looked at Sally Beauty Holdings’ ROCE trends, we weren’t very confident. Specifically, ROCE has declined from 28% over the past five years. However, Sally Beauty Holdings appears to be reinvesting for long-term growth. That’s because, although capital employed has increased, the company’s sales haven’t changed much over the past 12 months. It’s worth keeping an eye on the company’s earnings going forward to see if these investments ultimately contribute to its bottom line.

Our take on Sally Beauty Holdings’ ROCE

To summarize, Sally Beauty Holdings is reinvesting money into the business for growth, but unfortunately sales don’t seem to be growing that much yet. Investors also seem hesitant to see the trend accelerate, as the stock is down 28% over the past five years. Overall, the inherent tendency is not unique to multibaggers, so we think if that’s what you’re looking for, you might have better luck elsewhere.

There is one more thing to note. 1 warning sign Partnering with Sally Beauty Holdings, understanding this should be part of your investment process.

If you want to find solid companies with high earnings, check this out. free List of companies with good balance sheets and good return on equity.

Valuation is complex, but we help make it simple.

Please check it out Sally Beauty Holdings Could be overvalued or undervalued, check out our comprehensive analysis. Fair value estimates, risks and caveats, dividends, insider trading, and financial health.

See free analysis

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.