share price rises 26% but I don’t understand what it means")

Despite already showing good performance, Selecor Gadgets Limited (NSE:CELLECOR) shares are on a roll, up 26% in the past 30 days. Long term shareholders will be pleased to see the share price recover, as the stock has been roughly flat for the year since the recent surge.

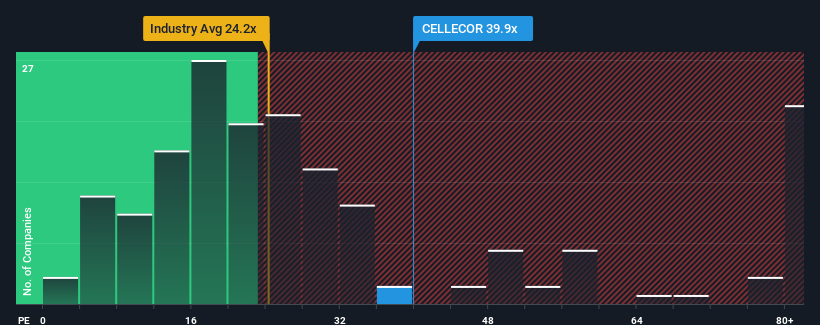

After such a big increase in its share price, Cellecor Gadgets, with a P/E ratio of 39.9, may be considered a stock to avoid, given that roughly half of Indian companies have a price-to-earnings (or “P/E”) ratio below 32. That said, we need to dig a little deeper to determine whether there is a rational basis for the increase in the P/E.

Cellecor Gadgets has been doing well lately, with revenue growing at a solid pace. Many expect the company to outperform most other companies in the coming period, which may be encouraging investors to pay a premium for the company’s stock. We really hope so; if not, we’re paying a pretty high price for no good reason.

Check out our latest analysis for Cellecor Gadgets

Want a complete picture of a company’s earnings, revenue, and cash flow? free A report on Cellecor Gadgets will help shed light on the company’s performance so far.

Does Cellecor Gadgets have enough growth?

Cellecor Gadgets’ P/E ratio is typical for a company that is expected to have solid growth and, more importantly, outperform the market.

Looking back, the company grew earnings per share by 30% last year, but EPS has barely grown in total compared to three years ago, which is not ideal, so shareholders probably wouldn’t be too happy with the unstable medium-term growth rate.

Compared to the market, which is expected to grow 25% over the next 12 months, the company’s momentum is weak based on its recent mid-year annual earnings results.

This information raises concerns that Cellecor Gadgets is trading at a higher P/E than the market. Most investors seem to be ignoring the fairly limited recent growth rate and hoping for an upturn in the company’s business outlook. Only the boldest would consider these prices sustainable, as a continuation of the recent earnings trend will likely ultimately weigh on the share price.

The last word

Cellecor Gadgets’ share price is being pushed in the right direction, but so is its price-to-earnings ratio. The power of the price-to-earnings ratio is not primarily as a valuation tool, but rather as a gauge of current investor sentiment and future expectations.

Our research into Cellecor Gadgets reveals that the company’s three-year earnings trend is worse than current market expectations, which is not impacting the high P/E as much as we would expect. At this point, we are concerned about the high P/E as this earnings performance is unlikely to support such positive sentiment for the long term. If the recent medium-term earnings trend continues, shareholders’ investments would be at significant risk and potential investors would be in danger of paying an excessive premium.

Before proceeding to the next step, 4 warning signs for Cellecor Gadgets (2 Makes us uneasy!) What we discovered.

If you are Concerns about the strength of Cellecor Gadgets’ businessTo see other companies you might have missed, be sure to check out our interactive list of stocks with solid fundamentals.

Valuation is complicated, but we can help make it simple.

investigate Selecall Gadget By checking our comprehensive analysis, you can see whether it may be overvalued or undervalued. Fair value estimates, risks and warnings, dividends, insider trading, financial strength.

View your free analysis

Have feedback about this article? Concerns about the content? contact Please contact us directly. Or email editorial-team (at) simplywallst.com.

This article by Simply Wall St is of general nature. We use only unbiased methodologies to provide commentary based on historical data and analyst forecasts, and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks, and does not take into account your objectives, or your financial situation. We seek to provide long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.

Valuation is complicated, but we can help make it simple.

investigate Selecall Gadget By checking our comprehensive analysis, you can see whether it may be overvalued or undervalued. Fair value estimates, risks and warnings, dividends, insider trading, financial strength.

View your free analysis

Have feedback about this article? Concerns about the content? Please contact us directly. Or email us at [email protected]